True ROI on rental property is more than just rent and loan payments. Here’s how you really measure it

September 10, 2018

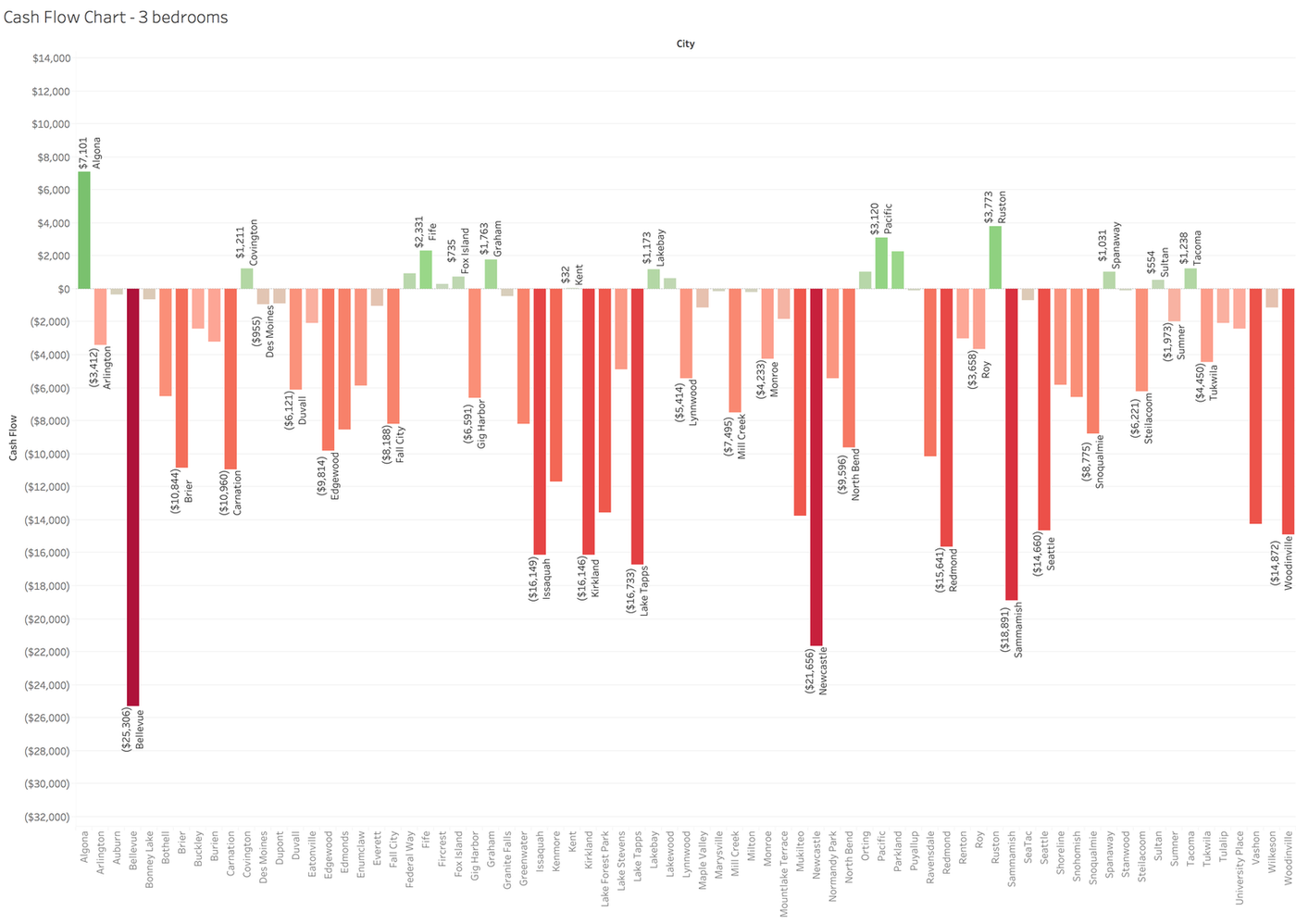

For real estate investors who are in the market for purchasing rental properties, it can be overwhelming to go through thousands of properties using online search platforms or inquiring with their real estate agents and peers. When properties are identified, the easiest and fastest way that investors use to make a decision is to calculate the loan payments, estimate the rent, then subtract the two and get a rough idea of whether it is cash flowing positive or not. In fact, they may sometimes go with their gut feeling and make these important decisions. A little more sophisticated investor may have a spreadsheet that may take into account taxes and some other factors. But is this a sure way of knowing whether these properties will make you money in the long run? After all, as an investor, you have a goal in mind that you are trying to reach, which is achieving a certain amount of passive income over a certain number of years. Having one badly performing property can wipe out the gains of others.

There are many factors that need to be considered when measuring the cash flow performance of residential investment properties.

Mortgage Interest Rate: The rates change over time, so its important to stay current. You may get them from your banker or search online (such as bankrate.com). This is used to calculate the monthly loan payments.

Property Tax Rate: Each county may have a different tax rate, so check with the county where you intend to purchase the investment property. If you cannot find this information, you may use 1% as an estimate.

Closing Costs: This is the fees that is paid at the close of the real estate transaction. These include costs like appraisal fees, credit report, escrow fees, insurance policies, outstanding taxes etc. You can use 2% as a good estimate.

Vacancy Rate: Vacancy rates are different for homes than apartments. Typically, plan on having the rental property to be vacant for 1 month (that is, 8%) every year, the time it takes to place a new tenant when the old tenant leaves.

Maintenance/Repair cost: Maintenance and repair costs are estimated as a percentage of purchase price. For newer homes, 0.25-0.5% of purchase price may be used. For older homes, you may go as high as 2%. For example, a newer home that has newer appliances, roof, furnace, heating and cooling systems (which cost more to repair), the only maintenance you may encounter is unexpected breakdown of an appliance, electrical or heating system etc. So, if this house is purchased for $250,000, budgeting $600-$1200 a year is appropriate. Note that typically, the tenants are responsible for cost of normal wear and tear, such as replacing light bulbs, fixing clogged sinks etc.

Insurance cost: This is the cost of landlord protection insurance which covers the structure of the building and liabilities. It is good practice to require tenants to get their own personal property insurance.

Property Management cost: If you plan to manage your own property, then this cost is zero. If you will be hiring a property manager, 8-10% of gross rent is a good estimate to use for the cash flow calculations.

Utilities: As a landlord, you may decide to pay for utilities ($100-$200 a month may be used as an estimate) or have your tenant pay in which case the estimate is zero.

HOA dues: Association dues are part of the operating expenses.

After deriving the income and expenses, you can produce a list of performance metrics that facilitates your buying decision:

Operating Expenses: These are all the expenses incurred for operating the property on a monthly or yearly basis.

Operating Expenses = Property tax + Maintenance/Repair + Insurance + HOA dues + Property Management + Utilities (optional)

Gross Scheduled Income (GSI): GSI is the total income generated by the rental property. This includes the rent and any other income such as parking, laundry machines, or any other service fees.

GSI = Rent + other income

Gross Effective Income (GEI): This takes into account the vacancy rate.

GEI = GSI – (GSI * vacancy rate)

Net Operating Income (NOI): The net income derived after all expenses are paid.

NOI = GEI – Operating Expenses

Cash flow: This is simply the net amount that you pocket after all expenses are paid (before taxes).

Annual Cash flow = NOI – Annual Mortgage payment amount

Capitalization Rate (CapRate): This is an investment criterion that evaluates the potential rate of return on the investment property.

CapRate = NOI / Property Value

Rent-to-Value Ratio: Some investors use this criterion to evaluate the property using the 1% Rule, meaning that the monthly rent should be at least 1% of the purchase price. For example, if the property is priced at $150,000, the rent should be minimum $1500/month.

Rent-to-Value Ratio = Monthly Rent / Property Purchase Price

Cash In: This is the total amount of hard cash that you invest when you purchase a property. It includes the down payment, improvements and may include closing costs (unless you include them in the loan payments).

Cash In = Down payment + Improvements + Closing Costs

Cash-on-Cash return (CoC): This is the return on the cash invested into the property based on the cash flow.

CoC = Annual Cash Flow / Cash In

Debt Coverage Ratio (DCR): Lenders use this metric to evaluate the ability of the buyer to pay back debt. It shows whether the income from the property will cover the mortgage payments. Anything under 1% means the property is negatively cash flowing.

DCR = NOI / Annual Mortgage payment amount

Net Income Multiplier (NIM): The NIM is the opposite of CapRate. It is useful to come up with a value of the property when compared with similar properties. Lower number compared to similar properties means a better investment.

NIM = Property Value / NOI

Gross Rent Multiplier (GRM): The GRM is a valuation metric that some investors use to make purchase decisions. It is relevant only when compared to similar properties. It does not consider the operating expenses. The lower the GRM, the better the property.

GRM = Property Value / GSI

If you consider all these factors and metrics before purchasing a property, it should give you the confidence on how profitable you will be in the long run. Although these calculations do not seem complicated, what becomes almost impossible is to run these for every single property in the market. That is the reason why investors use quick valuation methods like rent-to-value ratios and GRM which you don’t need spreadsheets for, but they do not provide the type of confidence that you can get by running a detailed analysis. You must be able to run various what-if scenarios. For example, what if you have to lower the rent, what will cash flow look like then. What if the maintenance cost of a certain property is higher than expected; what is the minimum cap rate I can expect, and so on. RealPeek is a decision-making tool that allows investors to perform such high volume cash flow analysis on thousands of properties at once and gain confidence so that they can make informed decisions.